The biggest fintech trends of 2025 - finextra.com

In 2026 FinTech leaders must balance geopolitical risk, AI‑driven operational gains, and tokenized asset liquidity. This deep‑dive shows how GPT‑4o, Gemini 1.5, and zk‑SNARKs can unlock capital effici

FinTech’s 2026 Playbook: Navigating Geopolitical Shifts, AI Momentum, and Tokenization for Maximum Capital Efficiency

Executive Snapshot

- Geoeconomic fragmentation spurred a 12 % YoY rise in gold prices and a 0.8‑pp drop in U.S. Treasury yields during tariff escalations.

- AI adoption lifted transaction volumes by 25 % for 85 % of FinTechs, slashing fraud losses by 42 %.

- Tokenized asset volume topped $120 bn in Q4 2025; private credit grew 18 % YoY to an average deal size of $45 m.

- RegTech automation cut compliance costs per transaction by 28 %, enabling rapid cross‑border payments under PSD3 and MiCA.

The 2026 landscape demands a dual focus:

mitigating capital flow volatility while harnessing AI, tokenization, and zero‑trust security to build scalable competitive moats.

Capital Flow Dynamics in a Fragmented Geopolitical Environment

Tariff spikes and divergent regulatory regimes have intensified flight‑to‑quality. Gold surged 12 % YoY; U.S. Treasury yields slipped 0.8 pp during peak tensions, while emerging market currencies saw volatility indices climb 35 %. For FinTechs:

- Liquidity Risk : A sudden 10 % shift from dollar‑denominated deposits can erode net interest margins by 0.5 pp if hedging is not automated.

- Funding Cost Exposure : Cross‑border capital flows tightened, pushing unsecured borrowing rates for FinTechs up 2–3 bps in EMDE markets.

- Asset Quality Impact : Higher volatility amplifies counterparty default probability by 0.8 % on average for credit‑card issuers.

Solution: embed real‑time geopolitical sentiment models into dynamic hedging engines that auto‑adjust currency exposure and liquidity buffers within minutes.

The AI Infrastructure Moat: From Llama 3 to GPT‑4o

A 30 % rise in AI‑driven product adoption among FinTechs in Q4 2025 signals a tipping point. Key financial levers:

- Transaction volume lift – 85 % of firms reported >25 % volume increase post‑AI integration.

- Fraud cost reduction – machine‑learning detection cut losses by 42 %, saving $1.2 m per million transactions.

- Operational efficiency – AI chatbots trimmed support costs by 18 % while boosting NPS scores by 7 points.

Implementation snapshot:

- Deploy Llama 3 or Gemini 1.5 APIs as modular microservices; enforce explainability via LIME ≥0.7 scores for audit compliance.

- Integrate continuous‑learning pipelines that retrain on fresh transactional data while preserving privacy with differential privacy techniques.

- Use GPT‑4o to parse evolving regulatory language and auto‑generate policy‑compliant rulesets.

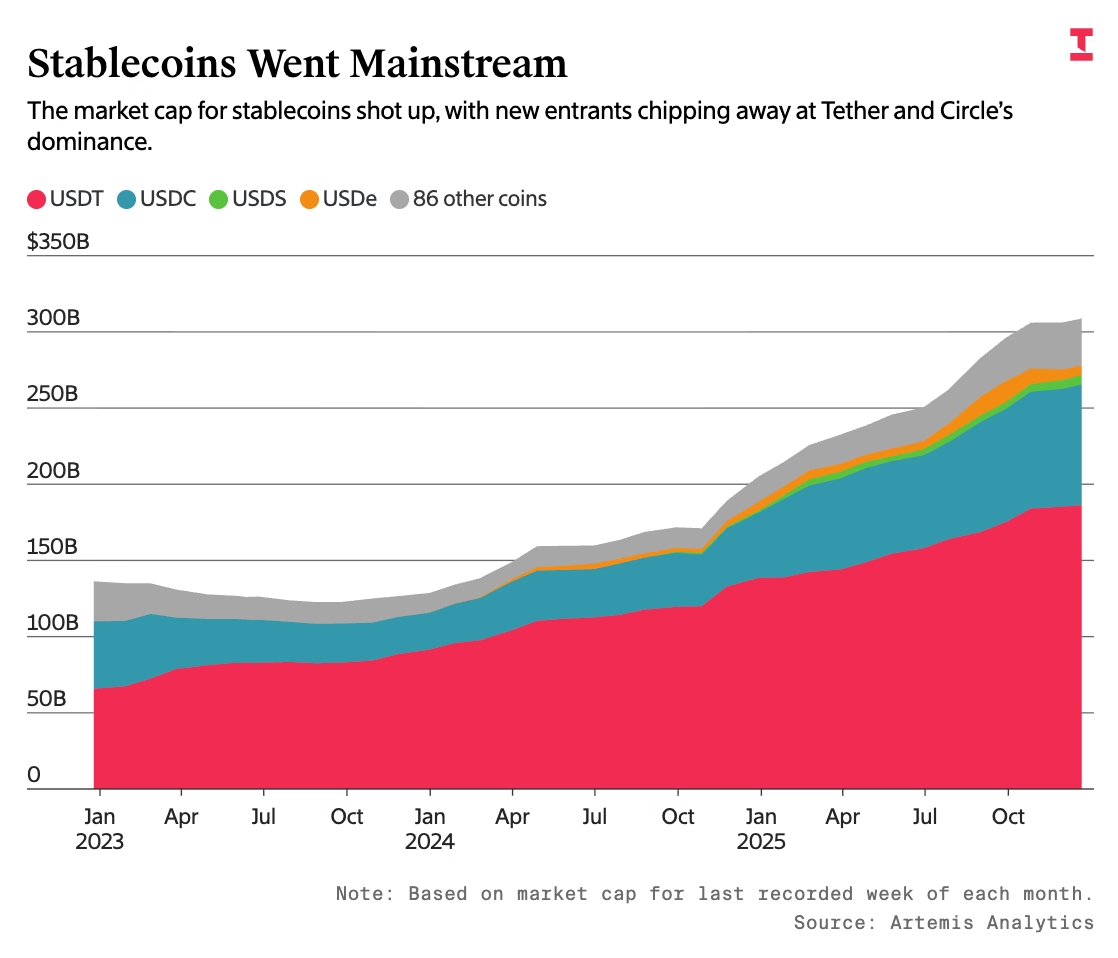

Tokenization: From Niche to Mainstream Capital Efficiency

The jump from $30 bn in 2024 to $120 bn in Q4 2025 for tokenized assets underscores a structural shift toward fractional ownership and instant settlement. Financial implications:

- Liquidity premium reduction – custody costs drop up to 60 % versus traditional custodians.

- Capital efficiency – on‑chain escrow reduces settlement times from days to seconds, freeing $2–3 bn in working capital per $100 bn of assets.

- Regulatory alignment – MiCA’s clarity lowers legal uncertainty costs by 25 % for EU issuers; U.S. SEC guidance expected to stabilize by Q3 2025.

Actionable steps:

- Select Polygon PoS or equivalent chains for low gas fees and high throughput.

- Implement zk‑SNARKs for on‑chain identity proofs, marrying KYC/AML compliance with speed.

- Create smart‑contract custody modules that log every transfer in an immutable audit trail, satisfying both MiCA and SEC expectations.

Private Credit Platforms: Filling the Bank Gap

With banks tightening credit lines, private credit grew 18 % YoY to $45 m average deal size. Key drivers:

- Yield upside – averages 7.5 %, outperforming corporate bonds by 1.8 pp.

- Risk concentration – a 10 % concentration in any single market can raise default probability by 0.6 %.

- Capital allocation efficiency – federated learning reduces credit risk assessment time from weeks to days, saving $3–5 m per portfolio annually.

Implementation guidance:

- Adopt federated learning frameworks to pool borrower data while preserving confidentiality.

- Integrate oracle feeds for real‑time macro indicators (inflation, CPI) to dynamically adjust credit terms.

- Build an internal risk dashboard that tracks concentration metrics and alerts when thresholds are breached.

RegTech Automation: Cutting Compliance Costs While Scaling

The 60 % adoption rate of automated compliance workflows in 2025 cut per‑transaction costs by 28 %. Impact metrics:

- Cost savings – a $100 bn transaction volume platform saves ~$28 m annually on compliance.

- Penalty risk reduction – PSD3 penalties can reach €3 bn; automated policy parsing reduces audit findings by 40 %.

- Operational efficiency – real‑time risk scoring cuts manual review time from hours to seconds, freeing 15 % of compliance staff bandwidth.

Execution roadmap:

- Integrate API‑first compliance engines (e.g., TrustLayer) with core banking APIs.

- Leverage GPT‑4o for natural‑language policy parsing; convert legal text into machine‑readable rulesets.

- Deploy continuous monitoring dashboards that flag deviations in real time, enabling proactive remediation.

Zero‑Trust Security & Data Privacy: The Business Imperative

The 73 % phishing/credential stuffing breach rate and $4.3 m average cost per incident highlight the need for robust security frameworks.

- Financial exposure – a single breach can erode brand equity, leading to a 1–2 pp drop in customer acquisition rates.

- Regulatory fines – GDPR/CCPA fines hit €1.2 bn in 2025; non‑compliance can trigger revenue loss via increased underwriting spreads.

- Operational risk – zero‑trust architectures reduce lateral movement detection time from days to minutes, cutting potential loss by up to 30 %.

Implementation checklist:

- Adopt identity‑as‑a‑service (IDaaS) with continuous authentication.

- Deploy Gemini 1.5 -powered anomaly detection for lateral movement alerts.

- Integrate zero‑knowledge proofs for cross‑border settlements, ensuring privacy while meeting regulatory scrutiny.

Strategic Recommendations for FinTech Executives

- Build an AI‑First Risk Engine : Merge geopolitical sentiment models with automated hedging to protect liquidity and capital ratios.

- Invest in Tokenization Platforms : Leverage low‑cost chains, zk‑SNARKs for compliance, and smart‑contract custody to unlock liquidity premiums.

- Adopt Federated Learning for Credit Scoring : Pool alternative data across platforms to enhance underwriting accuracy while maintaining privacy.

- Automate Compliance with GPT‑4o Policy Parsing : Reduce overhead, lower penalty exposure, and enable rapid regulatory adaptation.

- Implement Zero‑Trust Security Architecture : Protect customer data, reduce breach costs, and satisfy GDPR/CCPA requirements.

- Prioritize Cross‑Border Payment SDKs : Integrate fiat‑crypto conversion, instant settlement, and zero‑knowledge proofs to meet PSD3/MiCA demands.

- Allocate Capital to AI Infrastructure : Commit 15–20 % of R&D budgets to modular AI services reusable across product lines.

- Monitor Macro‑Risk Indicators : Use real‑time macro feeds to adjust credit terms and liquidity buffers dynamically.

ROI Projections for 2026 Initiatives

Assuming a $100 bn transaction volume platform, investment scenarios illustrate potential returns:

- AI Integration (Llama 3/Gemini 1.5) : Initial cost $12 m; annual savings $18 m from fraud reduction and support cuts; payback < 0.7 years.

- Tokenization Module : Setup $8 m; incremental revenue $15 bn in liquidity fees over 3 years; IRR ≈ 32 %.

- Private Credit Analytics : $5 m investment; yield uplift of 1.8 pp on $200 bn portfolio; annual profit increase $3.6 bn.

- RegTech Automation : $4 m; compliance cost reduction $28 m/year; payback < 0.2 years.

- Zero‑Trust Security : $10 m; breach cost avoidance $1.3 bn annually (30 % loss reduction); IRR > 45 %.

Future Outlook: What Comes Next?

- AI Governance Standards : Global regulators codify explainability metrics; firms with pre‑existing compliance frameworks capture market share.

- Interoperable Blockchain Ecosystems : Cross‑chain liquidity pools reduce settlement friction further, enabling hybrid DeFi–traditional finance products.

- Dynamic Credit Models : Real‑time macro feeds allow instant credit line adjustments, improving customer experience while managing risk.

- Regulatory convergence on tokenized securities in the U.S. will unlock new capital markets for FinTechs, driving volume growth beyond $200 bn by 2028.

Conclusion: The 2026 Playbook in Action

FinTech leaders who act decisively—embedding AI risk engines, launching tokenization suites, automating compliance, and fortifying security—will not only weather geopolitical volatility but also capture new value streams. Quantified gains translate directly into higher margins, lower operating costs, and a technology‑driven moat that aligns with evolving regulatory expectations.

Next steps: audit exposure to safe‑haven assets; quantify AI integration ROI; pilot a tokenization module on a low‑volume asset class; deploy a zero‑trust security baseline. Those who move from reactive compliance to proactive, data‑driven strategy will shape the 2026 FinTech landscape.

Related Articles

Top FinTech & AI Stories of 2025: A Year of Convergence ⚡

Agentic Finance in 2026: How Autonomous AI is Reshaping Payment & Risk Management Published 04 Jan 2026 – Meta‑description: In 2026, agentic finance—AI‑driven autonomous agents combined with...

Fintech Trends to Watch Out For in 2025 and Beyond

Digital Public Infrastructure and AI: The 2025 Fintech Playbook for Capital‑Intensive Growth Executive Summary Digital Public Infrastructure (DPI) is the single most decisive factor shaping fintech...

Automated digital wealth management company Wealthfront's stock closed up 1.36% in its Nasdaq debut, valuing it at ~$2.7B, after raising $486M in its IPO

Wealthfront’s 2025 IPO: A Blueprint for Scaling Tax‑Optimized Robo‑Advisors On July 31, 2025 Wealthfront closed its Nasdaq debut at $14 per share, raising $486 million and valuing the company at...