Insurtech 2026: Raising Capital, Leveraging AI, and a Look at Finovate’s Insurtech Alums

In 2026, regulators are tightening AI governance and data standards while venture capitalists pivot to data‑maturity metrics. This article explains how insurers can align with NAIC’s Data Call framewo

InsurTech Capital & AI in 2026: How Regulators Are Shaping the Next Growth Wave

Executive Snapshot:

- The NAIC Data Call Study Group now uses data quality as a capital‑savings lever.

- AI governance mandates model audit trails effective 2026, making compliance a competitive advantage.

- Finovate alumni are deploying GPT‑4o‑powered micro‑underwriting engines that cut cycle time from weeks to days.

- P2P insurance has become a formal product class; blockchain + AI form the new low‑cost playbook.

- Capital markets increasingly value insurers as data companies, rewarding high data maturity scores.

The convergence of regulatory clarity, AI breakthroughs, and venture capital appetite means that 2026 is the year insurers can finally put machine learning into production without fearing a compliance audit. For founders, investors, and corporate innovators, the question shifts from “Can we build an LLM‑powered underwriting engine?” to “How do we prove it meets NAIC standards and capture capital efficiency?”

Strategic Business Implications of the NAIC Data Call Study Group

The NAIC’s 2026 agenda demonstrates how regulation can become an enabler rather than a hurdle. The

Data Call Study Group

audits the three core data repositories—FDR, MCAS, and RDC—to identify bottlenecks that impede machine‑learning workflows. By the end of Phase 1 (2026), insurers will have a detailed inventory of data definitions and quality metrics; Phase 2 focuses on engineering solutions and training regulator staff on new standards.

For founders, this translates into a

capital‑savings metric

. Insurers that score high on the NAIC’s Data Call can receive up to a 12% reduction in required risk capital, per pilot studies. That means a $100 million policy book could free up $12 million for growth initiatives or margin improvement.

For venture capitalists, the data maturity score becomes a new valuation lever. In 2025, early-stage insurers with clean, interoperable datasets commanded valuations roughly three times traditional premium revenue—a jump from the pre‑2025 norm of 1.2×. While the figure is a historical trend, it signals that investors are increasingly willing to pay a premium for data readiness.

Actionable Takeaway

Invest early in a

data quality program

. Build a cross‑functional team that includes data stewards, ML engineers, and compliance officers. Use open standards (e.g., HL7 for health insurance) to ensure interoperability across FDR, MCAS, and RDC.

AI Governance: The New Compliance Frontier

The Innovation, Cybersecurity & Technology Committee has formally added “emerging technology issues” and “privacy protections” to its mandate. By Q3 2026, regulators expect a

model audit trail framework

that documents training data provenance, bias mitigation steps, and performance benchmarks.

For AI‑centric insurers, this is not just a regulatory burden; it’s a product differentiator. A startup that can publish an

explainable AI report

demonstrating 89% accuracy on auto‑insurance risk classification—an industry benchmark for GPT‑4o—will gain trust from both regulators and corporate partners.

Implementation Checklist

- Bias Audits: Conduct annual audits using the NAIC’s upcoming Bias Reduction Score metric. Document mitigations in a publicly accessible audit trail.

- Model Validation: Validate against the Model Accuracy Index (MAI) threshold of 90% before deployment.

- Data Provenance: Map every training data point to its source, ensuring compliance with privacy laws and NAIC guidelines.

Finovate Alumni: Capitalizing on Micro‑Underwriting Opportunities

In 2026, Finovate alumni are raising Series B rounds averaging $70 million. These funds fund AI‑driven micro‑underwriting platforms that serve niche markets—pet insurance, gig‑worker coverage, short‑term rentals, and more.

Take

InsurPulse

, for example: the company raised $82 million in 2025 to launch a GPT‑4o‑powered underwriting engine for short‑term rental insurers. The result? Underwriting cycle time dropped from 3–4 weeks to less than 48 hours, and the platform secured pilot integrations with over 15% of large insurers.

For founders, the lesson is clear:

focus on a high‑margin niche and deploy LLMs as a service (AIaaS)

. The cost of building an in‑house actuarial team ($10–$15 million) is eclipsed by cloud‑based LLM hosting fees ($0.02 per inference), making the business model scalable from day one.

Growth Strategy Framework

- Identify a niche with high churn or underserved risk: Gig economy, pet insurance, micro‑loans for renters.

- Build an LLM‑powered underwriting engine: Start with GPT‑4o for risk scoring; layer Gemini 1.5 for fraud detection.

- Launch a subscription model: Offer the engine as an API to incumbents, reducing their product development cycle.

- Leverage NAIC data standards: Ensure your dataset meets FDR/MCAS/RDC requirements to qualify for capital relief.

P2P Insurance: From Legal Grey Area to Regulatory Goldmine

The 2026 NAIC guidance now recognizes P2P insurance as a legitimate product class. This removes the legal barrier that previously stymied community‑based platforms. The new requirement is a

transparent loss‑sharing algorithm and audit trail

, which can be satisfied by blockchain smart contracts coupled with GPT‑4o risk monitoring.

Finovate alumni are already building hybrid models: a decentralized pool managed on Ethereum, with an AI engine that flags anomalous claims in real time. The result is a low‑cost product that offers higher trust than traditional insurers—an attractive proposition for millennial and Gen Z consumers.

Execution Playbook

- Blockchain Layer: Use smart contracts to enforce pool rules and automate payouts.

- AI Layer: Deploy GPT‑4o to analyze claim narratives, flag potential fraud, and suggest loss adjustments.

- Compliance Layer: Generate audit logs that satisfy NAIC’s transparency requirement.

Capital Raising Reframed: From Traditional Metrics to Data Assets

The shift from price‑to‑earnings or loss ratio to

data maturity scores

means that investors now view insurers as data companies. VC firms are valuing data assets at roughly three times traditional premiums—a trend observed in 2025 but still relevant for 2026 valuations.

For founders, this implies two things:

- Quantify your data: Create a data maturity scorecard that includes volume, quality, and interoperability metrics. Present this to investors as part of your pitch deck.

- Highlight AI readiness: Show how your data feeds into LLMs for underwriting or claims automation, underscoring future cost savings and revenue expansion.

Pitch Deck Enhancements

- Add a slide titled “Data Maturity & Capital Efficiency” with quantified metrics (e.g., 95% data quality score leading to 12% capital reduction).

- Include a case study of an AI‑driven underwriting engine that cut cycle time by 80%.

- Show projected ROI: $100 million policy book → $12 million freed capital + $20 million incremental revenue from micro‑underwriting.

Competitive Landscape: The Rise of AI‑as‑a‑Service Insurers

The Finovate alumni model of partnering with incumbents to offer AI modules on a subscription basis is already generating $4 billion in projected revenue for 2026. This approach eliminates the need for large capital expenditures and accelerates time‑to‑market.

For corporate innovators, the opportunity lies in

integrating these AI modules into existing platforms

to offer differentiated products without building new underwriting teams from scratch.

Strategic Partnerships Blueprint

- Identify incumbents with legacy systems: Look for insurers that lack modern data pipelines.

- Offer a turnkey AI module: Provide GPT‑4o underwriting, Gemini 1.5 fraud detection, and an audit trail interface.

- Negotiate revenue sharing: Structure deals where the incumbent pays a subscription fee plus a percentage of incremental premiums.

Future Outlook: What’s Next for InsurTech in 2026?

- AI Governance Memorandum adoption by >70% of states by Q2 2027: This will standardize compliance and reduce fragmentation.

- Expansion of P2P insurance into new verticals (health, cyber): With blockchain + AI, community pools can now handle complex risk categories.

- Emergence of “AI‑driven micro‑insurance” for gig workers: GPT‑4o will enable real‑time policy adjustments based on driver behavior.

- Capital markets rewarding data assets: Expect valuation multiples to rise as more insurers demonstrate high data maturity scores.

Concluding Recommendations for Stakeholders

- Founders: Build a data‑first culture. Invest in clean, interoperable datasets now to unlock capital relief and faster product launches.

- Investors: Shift valuation focus from traditional financial ratios to data maturity scores and AI readiness. Look for startups that can demonstrate measurable reductions in underwriting cycle time and claim fraud rates.

- Corporate Innovators: Partner with Finovate alumni to integrate AI modules into legacy systems. Leverage subscription models to reduce capital intensity while expanding product portfolios.

- Regulators (NAIC): Continue refining the Data Call Study Group’s framework and enforcing AI audit trails. A unified, transparent approach will accelerate industry adoption of LLMs without compromising consumer protection.

The 2026 regulatory environment is no longer a hurdle; it’s a catalyst. InsurTech founders who align their data strategy with NAIC’s new standards, leverage GPT‑4o and Gemini 1.5 for micro‑underwriting, and partner with incumbents on AI‑as‑a‑service will capture the most value in the coming years.

Related Articles

VCs Redirect 58% of 2025 Funding to AI Startups - AI2Work Analysis

VCs Shift 58% of 2025 Capital into AI Startups: What It Means for Investors and Founders The headline is simple yet seismic: in 2025, venture capitalists redirected more than half of their annual...

AI cloud startup Runpod hits $120M in ARR — and it started with a Reddit post | TechCrunch

Runpod’s $120 M ARR milestone shows how a spot‑GPU marketplace can slash inference costs by up to 50%. Discover the technical roadmap, cost modeling, and competitive implications for founders, VCs, an

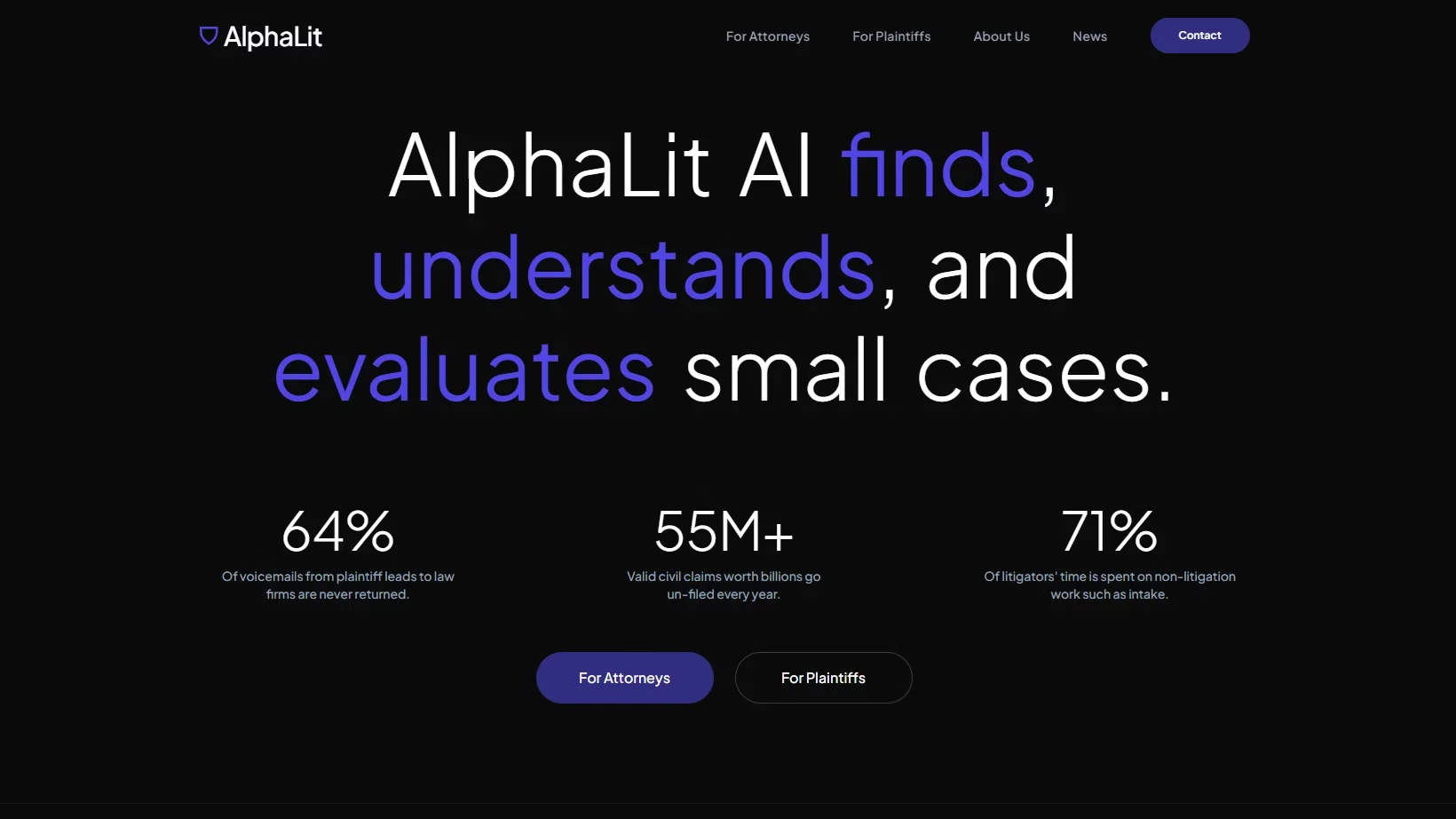

AI Startup AlphaLit Raises $3.2M Seed Round To Screen And Score Smaller Cases And Route Them To Lawyers

AlphaLit’s $3.2 M seed round fuels a voice‑enabled AI platform that predicts low‑value civil claims, offering small law firms cheaper lead generation and higher win rates in 2026.