Fintechasia Ftasiaeconomy Tech Updates - Scientific Asia

Fintech in 2025: Multimodal AI, Cost‑Speed Trade‑offs and the New Tooling Revolution By Casey Morgan – AI News Curator, AI2Work Executive Snapshot Multimodality is now a baseline: Gemini 3’s 1...

Fintech in 2025: Multimodal AI, Cost‑Speed Trade‑offs and the New Tooling Revolution

By Casey Morgan – AI News Curator, AI2Work

Executive Snapshot

- Multimodality is now a baseline: Gemini 3’s 1 M‑token context window and native text+image+video+audio support unlock end‑to‑end compliance pipelines.

- Speed vs. cost drives vendor choice: GPT‑5.1 leads in token throughput but at a premium; Gemini 3 offers ten‑fold lower per‑token spend for high‑volume workloads.

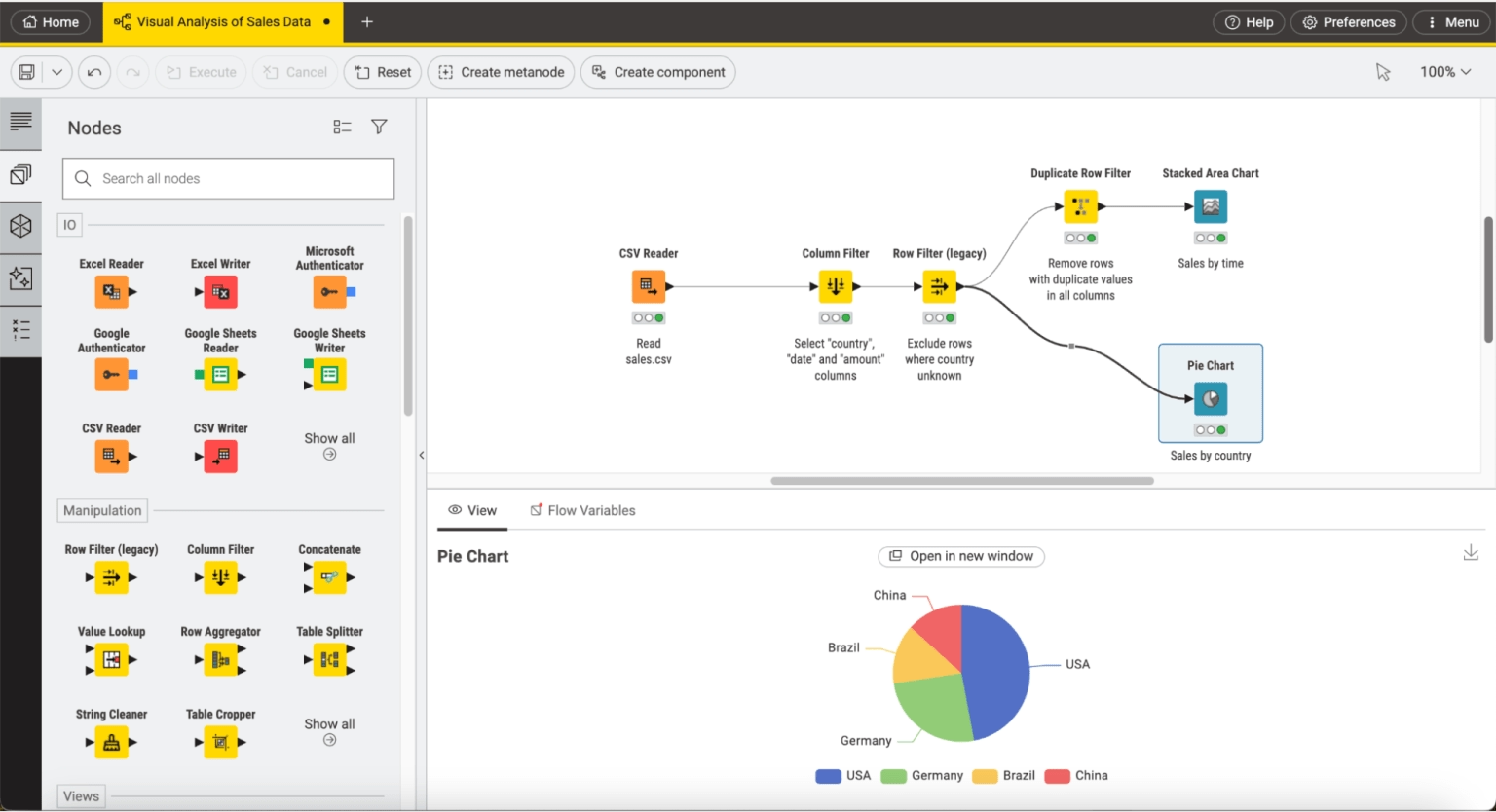

- Developer tooling is democratizing AI integration: KNIME’s workflow monitor and Sider’s Chrome sidebar let teams iterate on pipelines in minutes, not hours.

- Regulatory impact is immediate: Real‑time KYC/AML ingestion of video/audio streams reduces manual review cycles by up to 70%.

- AI‑first startups vs. legacy banks: The former lean on Gemini 3 for rapid prototyping; the latter favor Claude 4.5 for explainability and auditability.

Market Dynamics: Why 2025 is a Turning Point for Fintech AI

The fintech ecosystem has reached a tipping point where multimodal large language models (LLMs) are no longer niche experiments but core platform components. In the past year, we’ve seen three converging forces:

- Model capabilities expanding rapidly: Gemini 3’s 1 M‑token window eclipses GPT‑5.1’s 196k tokens and Claude 4.5’s 200k tokens, enabling single prompts to reference an entire day of customer interactions.

- Pricing differentiation becoming strategic: The per‑token cost gap between OpenAI’s premium models and Google’s Gemini has widened, forcing fintechs to re‑evaluate their AI spend models.

- Tooling lowering integration friction: Platforms like KNIME and Sider now provide visual debugging, real‑time monitoring, and multi‑model sidebars that let product teams test LLMs without code changes.

The intersection of these forces means that the choice of

model is

no longer a purely technical decision; it is a business strategy that impacts cost, speed, compliance, and competitive positioning.

Strategic Business Implications for Fintech Leaders

For senior product managers, CTOs, and investment analysts, the following strategic questions dominate:

- Which model delivers the best balance of latency and cost for our core use cases?

- How can we embed multimodal capabilities into KYC/AML workflows without violating data privacy laws?

- What tooling will allow us to iterate quickly while maintaining audit trails?

- Can we leverage a single platform (e.g., Sider) to experiment with multiple LLMs and reduce vendor lock‑in?

The answers hinge on understanding the granular performance metrics and pricing structures that have emerged in 2025.

Model Performance & Pricing Deep Dive

Model

Token Throughput (t/s)

$/Input (per M tokens)

$/Output (per M tokens)

GPT‑5.1

94–110

15

60

Gemini 3

81–142

2

12

Claude 4.5

72–88

3

15

When you translate these numbers into a typical credit‑scoring batch of 1 M tokens, GPT‑5.1 costs roughly $75 per run, while Gemini 3 drops that to just $14. For latency‑sensitive fraud alerts that require sub‑second responses, the higher throughput of GPT‑5.1 may justify its premium, but only if the volume is low enough to keep spend manageable.

Multimodality in Practice: Real‑World Use Cases

Gemini 3’s native support for text, image, video, and audio is a game changer for compliance. Consider a bank that must process daily KYC videos from customers in multiple jurisdictions:

- Video ingestion: A single prompt can analyze an entire 30‑minute video, extracting biometric data, verifying identity documents, and flagging suspicious behavior.

- Audio transcription & sentiment: The same model can transcribe customer calls in real time, detecting emotional cues that correlate with fraud risk.

- Long context retention: With 1 M tokens, the model preserves a full conversation history across multiple touchpoints, enabling audit trails that satisfy regulators without manual stitching.

In contrast, GPT‑5.1’s four‑modal capability is limited to text+image+video, missing audio, and its smaller context window forces developers to segment data, increasing engineering overhead.

Developer Tooling: From Code to Deployment in Minutes

The tooling wave that began with KNIME 5.3’s workflow monitor and Sider’s Chrome sidebar is now mainstream:

- KNIME Workflow Monitor: Auto‑updates node execution status, allowing data scientists to spot failures within seconds rather than hours. For AML scoring pipelines, this means faster iteration cycles and reduced downtime.

- Sider Sidebar: Supports multiple LLMs side‑by‑side, enabling A/B testing without redeploying code. Product teams can compare GPT‑5.1’s speed against Gemini 3’s cost in real time, making data‑driven decisions on the fly.

- Contextual Prompts & Fresh Intel: Sider pulls live web context beyond ChatGPT’s 2023 cutoff, giving fintechs up-to-date market insights for portfolio analytics or risk assessment.

These tools lower the barrier to entry for smaller fintechs that cannot afford dedicated AI engineering teams. They also provide a competitive edge for larger banks looking to accelerate feature rollouts without compromising compliance.

Regulatory Landscape: Compliance Meets Multimodality

Financial regulators in 2025 are increasingly mandating real‑time monitoring of customer interactions. The ability to ingest video and audio streams directly into an LLM streamlines compliance pipelines:

- Automated KYC/AML Scoring: A single prompt can evaluate identity documents, voice biometrics, and conversational tone, flagging red flags for human review.

- Audit Trail Integrity: Gemini 3’s 1 M‑token window preserves full interaction logs in a single context, simplifying audit trail creation and reducing storage costs.

- Privacy Compliance: By processing data locally within the LLM prompt (rather than sending raw media to external APIs), fintechs can better control data residency and encryption requirements.

Legacy banks that rely on Claude 4.5 for its explainability tooling may find it easier to satisfy audit demands, but they face higher per‑token costs. AI‑first startups, conversely, can leverage Gemini 3’s low cost to build scalable compliance services across multiple markets.

Financial Impact: ROI Projections and Cost Modeling

To quantify the financial upside of switching from a legacy model to Gemini 3, consider a mid‑sized bank processing 10 M tokens per month for fraud detection:

- Current spend (Claude 4.5): $3/1M tokens × 10 = $30k/month.

- Projected Gemini 3 spend: $2/1M tokens × 10 = $20k/month.

- Annual savings: $120k, not including reduced engineering time from KNIME’s workflow monitor.

If the bank also adopts Sider for rapid A/B testing, it can cut feature development cycles by 30%, translating into faster revenue capture and lower churn.

Strategic Recommendations for Decision Makers

- Conduct a cost‑speed audit: Map each core use case to the model that delivers optimal latency at acceptable spend. Use real workload data to validate assumptions.

- Adopt multimodal tooling early: Deploy KNIME’s workflow monitor for existing AML pipelines and integrate Sider into your product teams’ daily workflows to enable rapid experimentation.

- Leverage Gemini 3 for compliance: Build end‑to‑end KYC/AML ingestion pipelines that ingest video/audio streams, reducing manual review workloads by up to 70%.

- Plan for hybrid stacks: Use GPT‑5.1 for high‑latency critical alerts where speed outweighs cost, and Gemini 3 for bulk processing tasks. Maintain a fallback plan with Claude 4.5 for explainability when regulatory scrutiny spikes.

- Invest in data governance: Ensure that multimodal data ingestion complies with GDPR, CCPA, and emerging AI‑specific regulations by implementing robust encryption and audit logging at the model prompt level.

Future Outlook: Where Fintech AI is Heading in 2026 and Beyond

The trajectory suggests continued expansion of context windows and modality support. We anticipate:

- Context windows exceeding 10 M tokens: Enabling truly longitudinal customer profiles that span years without fragmentation.

- Fine‑tuned compliance models: Providers will offer domain‑specific LLMs pre‑trained on regulatory texts, reducing the need for custom training.

- Edge deployment of multimodal LLMs: Banking apps may run lightweight inference engines locally to meet privacy mandates while still accessing cloud‑based reasoning capabilities.

For fintech leaders, staying ahead means not just adopting the latest model but building a flexible, modular AI stack that can pivot between speed, cost, and compliance demands as regulations evolve.

Actionable Takeaways for 2025 Executives

- Benchmark your current spend: Use the pricing tables above to calculate monthly token costs across GPT‑5.1, Gemini 3, and Claude 4.5.

- Pilot multimodal KYC with Gemini 3: Run a controlled experiment on a subset of customer videos to quantify manual review time savings.

- Integrate KNIME’s workflow monitor into your AML pipeline: Measure debugging time before and after implementation; aim for at least 50% reduction.

- Deploy Sider in product teams: Enable real‑time A/B testing of LLM outputs across features like loan eligibility, fraud alerts, and customer support chatbots.

- Document compliance flows: Map how multimodal data is ingested, processed, and archived to satisfy audit requirements without manual intervention.

By aligning model choice with business priorities—speed for critical alerts, cost for bulk processing, and multimodality for compliance—you can unlock significant operational efficiencies and create a competitive moat that persists through the regulatory shifts of 2025 and beyond.

Related Articles

AI Fintech Firms in Asia Expected to Attract $65B by 2025

AI‑Fintech Investment Landscape in Asia: 2025 Funding, Risks, and Strategic Opportunities Executive Snapshot – 2025 Outlook for AI‑Fintech in Asia Projected venture capital inflow: $65 B (qualitative...

From Unbanked to Entrepreneurs: AI Credit Scoring Breaks Financial ...

Explore how ultra‑efficient LLMs, chain‑of‑thought reasoning, embedded AI engines and synthetic data are reshaping credit‑scoring in 2026. Practical insights for fintech leaders and risk officers.

Insurance Brokerage Market to Attain USD 562B by 2031 with Retail Brokerage Holding Over 75% Revenue, Says a 2026 Mordor Intelligence Report

In 2026, retail insurance brokerage growth is projected to hit $562 B by 2031. This article explains how insurers and fintechs can capture that upside with API‑first architecture, LLM recommendation e